Pricing a home is more complicated than simply comparing the list price to the sales price. Clients often ask me how much they should pay for a home, and I tell them, “It depends on how much it’s worth!” For example, if a house is listed at $450,000 and you get it at $400,000 that may seem like a good deal…but not if the market data says it’s only worth $350,000. (I’m using large numbers here to make the point.) Similarly, if a house is listed at $450,000 and you get it for $450,000, but the market data says it’s actually worth $500,000…then you got a good deal, even though you paid “full price.” See what I mean?

By the way…that new home specialist at the builder’s model home you like will tell you that the $440K model home was originally listed at $520K…sounds like a great deal, right? But they won’t tell you that the last five homes they sold, with that exact floorplan, had an average sales price of $400K. But I will! I’m looking out for you…not the builder.

Home Value Is Not About Price Per Square Foot

Pricing a home is complicated because real estate market data is changing every month…so home values are changing every month as well. In addition, there is not one price/sf price for an entire neighborhood. Smaller homes in the same neighborhood will typically have a higher price/sf than larger homes in the same neighborhood. Homes with swimming pools and water view lots are generally worth more in the same neighborhood than homes that don’t have those features. Three-car garage homes are worth more than two-car garage homes in the same neighborhood.

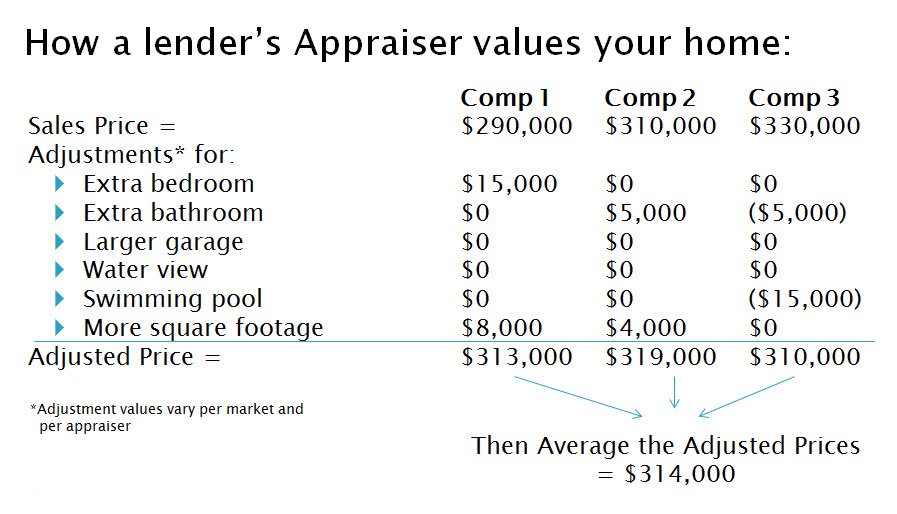

Pricing a home correctly is complicated…you can’t just work off of averages or price/sf. There is no “Kelly Blue Book” value for homes! When determining the value of a home, you should compare at least three to five recently Sold price (not asking prices) for homes that are comparable to the house you want. Comparable means the houses are all within the same size-range (+/- 10%sf), have a similar number of bathrooms, have similar garage sizes, have similar types of amenities and lot types, etc. Usually you will not find three to five homes that are exactly the same as the subject property, so adjustments must be made to the prices, and then the adjusted prices are averaged out. This gives you a good idea of a home’s current market value. See the example below.

By the way, cosmetic items such as granite counter tops, hardwood floors, updated light fixtures, special colors of paint…those items do not add value to a home. Appraisers do not make adjustments for most cosmetic items.

New Construction Homes Cost More Than Comparable Resale Homes

New construction homes in a neighborhood make pricing a home correctly more challenging. Technically speaking, investing in a home is very different from investing in an automobile. Homes and real estate are generally “appreciating assets” while cars are generally “depreciating assets.” However, trust me when I tell you that no home buyer on the planet is going to pay the same price for a “used” one-year old home when they can buy a “fresh,” brand-new, never lived in home…where they get to choose all the finishes (paint colors, floors, counter tops, cabinets, etc.). Buyers like that “new home smell” just the same as they like that “new car smell.” And they are willing to pay a premium for the “new home smell” just like they are willing to pay a premium for the “new car smell.”

We all know a car loses value the minute you drive it off the car lot. Likewise, that a new construction home typically loses its value (at least in the short run) the minute that you move in. So do not compare new construction prices with a resale home prices when determining value.

And be prepared to sell your home for less than you paid for it if you bought it from a builder…at least until the builders move out of the neighborhood (and no new construction homes are available) or at least five years (or more) have passed since you bought it from the builder. It is almost impossible to compete on price with home builders when you are selling a resale home. They offer lots of “buyer incentives” to entice buyers to purchase…and they can offer a buyer something you can’t…a never-lived-in-home.

It can be hard to determine what new construction homes are selling for because builders do not always list them on the MLS. Since Texas is a non-disclose state, home builders can sell homes without ever reporting them to the MLS. This often conceals the fact that homes lose value after they are purchased by a builder.

I know that some home sellers think their home is “better than new” because they have done this and that to the home. Home sellers like to price a home based on new construction home prices. But just like a used car, a used home is not usually worth as much to a buyer as a new construction home.

Home Should Appraise for Sales Price

If you are like most home buyers, you are going to get a loan in order to buy a home. That means the lender’s appraiser is going to have a say in how much you can pay for a home. This is something that home buyers and sellers have to be reminded about. It really doesn’t matter if you are willing to pay $450,000 for a house if the lender’s appraiser says it’s only worth $420,000…unless you want to pay the $30,000 difference at Closing.

Remember that a lender is making an investment in you and your home when they loan you money to buy a house. They want to make sure the home is a good investment. They don’t want to invest more than the item is worth. Always keep this in mind when you are applying for a loan.

Always make sure you have a way to get out of the deal if the home doesn’t appraise for the sales price. That will give you leverage to renegotiate the price if the appraisal comes in too low. If you have a back-out addendum in place, and the appraisal comes in too low, then you have four options:

- Get the Seller to come down in price to the appraised value

- Meet the Seller somewhere in-between the sales price and the appraisal price (but you will have to pay your share of the difference at Closing)

- Pay the difference between the sales price and the appraisal value at Closing…on top of your other down payment and Closing costs

- Back out of the deal (but then you will not get back all the money you spend on inspections, appraisal, etc.)

Some people think they will be able to terminate a transaction if the appraisal comes in too low because they believe a lender will not approve the loan in that case. This is not, necessarily, true. If you have enough cash on hand to pay the difference, then the lender may still approve the loan.

Tax Appraised Values Do Not Equal Market Value

Pricing a home based on the “tax rolls” and tax appraised values does not work in Texas. Tax appraised values are usually not accurate for market value in this state. The following short video proves that the tax appraised value is usually (not always) lower than the market value.

Plus, Texas is a non-disclose state and only members of the MLS have actual sales data.

And even Zillow only gives themselves 1-star on their Zestimate’s accuracy (see here).

Zillow’s algorithm was a huge failure with their iBuyer program! Why would anyone depend on a Zestimate?!

There is a method for doing a proper Comparative Market Analysis for a home that is similar to how a lender’s appraiser is going to determine a home’s value. Hire an experienced agent who knows what they are doing!

As your Buyer’s Agent, when you find a home you want to make an offer on, I do a complete CMA (Comparative Market Analysis) and provide you with the data that I have, to determine the realistic and accurate price for a home. This method is similar to how lender’s appraisers value a home. That way you don’t find yourself wasting a lot of time on a home that will not appraise for sales price.

Read more about “Buyer’s Agents”: The Agent Showing You Houses May Not Be Your Agent

Negotiating Price When It’s Too High

Often times a home is listed at a price that is considerably more than the CMA value. For example, a home that just hit the market may be listed at $550,000 and the CMA, which is based on comparable homes SOLD in the past six months) says it is only worth $500,000. But you, the Buyer, really want the house. What do you do? Well…

Neither the Buyer’s Agent or the Listing Agent can make a seller accept your reasonable offer. And if the house just hit the market, then it’s possible that the seller hasn’t “come to their senses” yet. Sometimes it takes time for a home seller to see that their home isn’t worth what they want for it. If the house sits on the market for months, then sellers either decide to lower the price (hopefully) or they take the home off the market, because they find out they can’t get what they want for it at the current time. (So they will wait.)

I have seen it time and again where a Buyer’s Agent shows the Listing Agent their data for the $500,000 offer and it doesn’t matter…until months go by. Then, eventually, the Seller finally sells the home at the price you offered (or lower)…after letting it sit on the market for 6 months. It is often the case that only TIME can motivate a seller to accept a reasonable offer.

So what do you do if you really want a house that is overpriced?

- Do you have time to wait? If so, give it a month or two and hope that another buyer doesn’t beat you to it. If you don’t have time to wait, then move on and find another home.

- Pay the higher price. Sometimes it is worth paying more for a house to get what you want, when you want it. And besides…paying a higher price helps raise the prices in the neighborhood…thereby increasing the value of your investment.

- Take a risk and offer the price the seller will accept while hoping the appraisal will come in low so you can renegotiate. Use the lender’s appraisal as your “checks and balances” for the price. This strategy can only work if you have the right to back out of the transaction if the appraisal comes in low.

Sometimes an appraisal comes in much higher than what a Buyer’s Agent thinks the house will appraise for. This may be because the market has changed in the 4-6 weeks between the time the agent did the CMA and the time the appraisal is done..and more homes sold in that time. Or sometimes it seems that appraisers choose odd “Comparables” to make the appraisal come in higher (or lower). You just never know what a lender’s appraiser will do when valuing a home.

Negotiating Tips for Buyers

Here are some tips to help with negotiations:

- Don’t let yourself “fall in love” with a house, making detailed plans for remodeling and decorating, before you have an executed contract. If you are emotionally attached to the home, then it will be harder for you to walk away from an over-priced home.

- Don’t expect to get a seller to go down substantially in price when the house has only been on the market for a few weeks. Be willing to pay a reasonable price instead of getting a “killer deal” on a house that just hit the market.

- Don’t low-ball a house in a HOT market when you may get in a competitive situation with other buyers. Be willing to pay a reasonable price (or slightly more) because other buyers will be willing to do so.

There is a funny saying in real estate: “You can’t fix stupid.” That’s just an irreverent way of saying that your Buyer’s Agent can’t prevent other buyers from overpaying for a home. Cash buyers commonly pay way too much for a home because they don’t have a lender’s appraisal holding them back. And you don’t know what the other buyer’s circumstances and motivation are…maybe they are too desperate to be conservative about price.

- Always consider your “next best alternative” when making pricing decisions. If you are desperate to get a home because you have to move in six weeks, and you have been looking for several months without finding anything else that you like, then be willing to pay more to get what you want. Likewise, if you are not being forced to move in a short-time frame, or you have seen lots of other homes that you like, then you can be “stricter” with the price you pay for a house.

- Do not take the CMA value of a home and then subtract from it all the cosmetic changes (paint, flooring, landscaping, pool, etc.) that you want to make to the home. It doesn’t work that way. Cosmetic items do not, generally, effect the value/price of a home.

- Remember that both CMAs and Appraisals are opinions of market value. If you have three different appraisers do an appraisal on the same home at the same time, you will probably end up with three, different values.

- Always remember that the price you pay effects the prices in the neighborhood where you are buying and investing. Driving too hard a bargain on your future home can have a negative impact on your home’s value too.

How’s the Katy Real Estate Market in 2022?

Get the Report!

What’s Included

What’s Included

- Ten-year trend of median sales prices by ZIP Code and neighborhood…so you have a baseline in determining a home value.

- Ten-year trend of sales volume by ZIP Code and neighborhood…so you can see which are the most popular neighborhoods.

- Ten-year trend of median Days on Market by ZIP Code and neighborhood…so you can see how long it takes to sell a home in each area.

- List of the most popular neighborhoods in the Katy area…see what neighborhoods are HOT!

- List of the neighborhoods by price (high to low) in the Katy area.

- Detailed market data on the most popular Katy neighborhoods

|

Download the Report!

|

Buying & Selling Real Estate Is a Huge Investment

Don’t You Deserve a Five Star Real Estate Agent?

Sheila Cox

832-779-2890

REALTORS DON’T “JUST” SELL HOUSESReal estate agents don’t “just” sell houses; we sell a SERVICE to effectively guide home buyers and sellers through the entire real estate transaction, which usually takes several months. We are more like real estate consultants than we are salespeople. That’s probably why 86 percent of all home buyers and sellers choose to hire a real estate agent when buying or selling a home! Buying or selling a home is not like buying or selling a TV, a computer, or a car. You can’t buy/sell a home on the Internet with a couple of clicks. There are MANY legal aspects, deadlines, and requirements that most people are not trained to handle. What’s more…mistakes along the way can cost you thousands and even hundreds of thousands of dollars. The financial risk is much greater than just about anything else you may buy.

Please read the list of my value-added services for home buyers |

FREE GUIDES & REPORTS by Sheila Cox, Five Star Realtor

Click Image Below to Download a Guide or Report

![]()

View Helpful Videos on Sheila’s YouTube Channel

Why You Should Hire Sheila Cox As Your Agent

Integrity—I promise to give you candid opinions on all homes and areas so you can make the best decisions. I won’t ignore potential defects that can cost you money, or effect your resale value, in the future…I point them out to you! My job is to protect you, as much as possible, from defective homes while helping you make a sound financial investment. You will get more REAL info from me regarding homes/neighborhoods than you ever had before! (Read client testimonials)

Integrity—I promise to give you candid opinions on all homes and areas so you can make the best decisions. I won’t ignore potential defects that can cost you money, or effect your resale value, in the future…I point them out to you! My job is to protect you, as much as possible, from defective homes while helping you make a sound financial investment. You will get more REAL info from me regarding homes/neighborhoods than you ever had before! (Read client testimonials)

Local Area Expertise—This isn’t just my business…it’s where I work and live (for 20+ years) so I really know the area. I will help you narrow your options and find the best neighborhood for you based on your specifications. For long-term resale value, the neighborhood you choose is just as important as the home you buy. (Download my Ultimate Katy Guide)

Great Pricing Data—I will give you the most in-depth data you have ever seen…to help you make the wisest decisions. This includes a professional CMA when you are ready to purchase a specific home…so you don’t pay too much. You can’t get this level of pricing information anywhere else. (Also see Pricing a Home Correctly)

Premium Customized Home Searches—Yes, you can search on your own, but no other home search available can filter down to the school level…and filter out the subdivisions that may be known to flood. Plus my search includes “Coming Soon” homes not listed on other websites. (Request a Premium Customized Home Search)

Video Home Tours—If you or your spouse lives out of the state or country, then you will enjoy my detailed video home tours. I have sold multiple homes to out-of-area clients “site unseen” by providing High Definition video walkthroughs of potential homes. My videos show front and back yards, closets, pantries, laundry rooms, and the garage…as well as the entire home. This gives you a complete picture of the house (unlike Matterports). I also point out any potential defects or deferred maintenance that I see. (view sample video walkthrough)

Easier Process—Moving your family (and possibly changing jobs) is stressful enough. I’m your transaction manager and will guide you, step-by-step, through the process so you never miss an important deadline. I assist with inspections, repair negotiations, home warranties, HOA compliance inspections, hazard insurance, surveys, appraisals, title commitment, home warranties, title commitment, and more. (Get Details of My Value-Added Services)

Client Reviews of Sheila

Connect With Sheila